Global Markets Watch Japan Rate Shift as UK and Canada Consumers Slow Spending

Global markets are ending the year focused on two closely connected themes, central bank policy shifts and the health of consumer spending. Developments in Japan, the United Kingdom, and Canada highlight how policymakers and households are responding to higher prices, rising interest rates, and uneven economic growth.

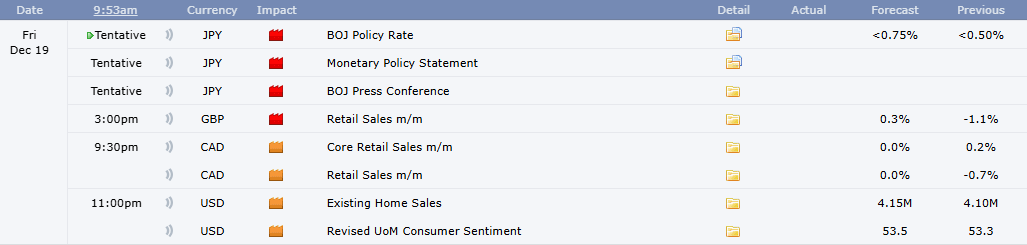

In Japan, attention is firmly on the Bank of Japan as it prepares to raise interest rates to their highest level in 30 years. The central bank is widely expected to lift its short term policy rate to 0.75%, marking another step in its gradual move away from years of ultra loose monetary policy. Inflation has stayed above the Bank of Japan’s 2% target for 44 straight months, driven mainly by higher food costs and a weak yen. At the same time, wage growth has improved, supported by labor shortages and strong pay agreements, giving policymakers confidence that inflation is becoming more sustainable rather than temporary.

A rate hike would reinforce Japan’s unique position among major economies. While the United States and parts of Europe are moving closer to easing or holding rates steady, Japan continues to tighten. This policy divergence has helped shape currency markets, where higher Japanese rates are expected to support the yen over time and limit further increases in import driven inflation. However, the timing is sensitive, as Japan’s economy remains fragile. Revised gross domestic product data showed that economic output contracted more than initially estimated in the third quarter, highlighting the risk that higher borrowing costs could weigh further on growth.

Because markets have largely priced in the rate increase, the focus is shifting to the Bank of Japan’s guidance on what comes next. Investors will be listening closely for comments from Governor Kazuo Ueda on the pace of future hikes and on the so called neutral rate, which is the level of interest rates that neither stimulates nor slows the economy. The central bank has previously estimated this range at between 1% and 2.5%, but officials have acknowledged that the true level is difficult to pinpoint. Any direct remarks on the yen’s weakness could also influence market reactions, as authorities remain wary of excessive currency declines that raise household costs.

While Japan looks toward tighter policy, the United Kingdom and Canada are offering insight into how consumers are coping with existing financial pressure through retail sales data. In the United Kingdom, retail sales over the past 12 months have been uneven. Volumes have generally grown only modestly on a year-on-year basis, reflecting cautious spending behavior as households deal with high living costs and lingering uncertainty about income and taxes. Monthly data have shown swings between gains and declines, suggesting that shoppers are timing purchases carefully and responding to promotions rather than spending freely. Over the year, categories such as household goods have provided some support, indicating that major purchases have not disappeared entirely, but overall momentum remains weak.

Canada’s retail sales story has also been marked by volatility. Earlier in the year, sales were supported by strong demand for motor vehicles and other big-ticket items. More recently, however, data showed a pullback in overall sales, driven mainly by lower vehicle purchases and softer demand across several sectors. When volatile categories such as gasoline and motor vehicles are excluded, underlying sales have been relatively flat, pointing to stable but subdued consumer demand. Regional data suggest that most provinces experienced declines, although some areas recorded gains tied to specific sectors.

Looking ahead, expectations for the latest retail sales releases in both the United Kingdom and Canada are modest. Analysts generally anticipate limited improvement, with consumers continuing to feel the effects of higher interest rates and past inflation. This cautious spending environment stands in contrast to Japan’s push toward policy normalization, underscoring how different economies are responding to similar global pressures.

Analysis by Coach Angel

——

Disclaimer: Investing is risky. Investors should study the information before making investment decisions