Global PMI Data Highlight Gradual Expansion Across Key Economies

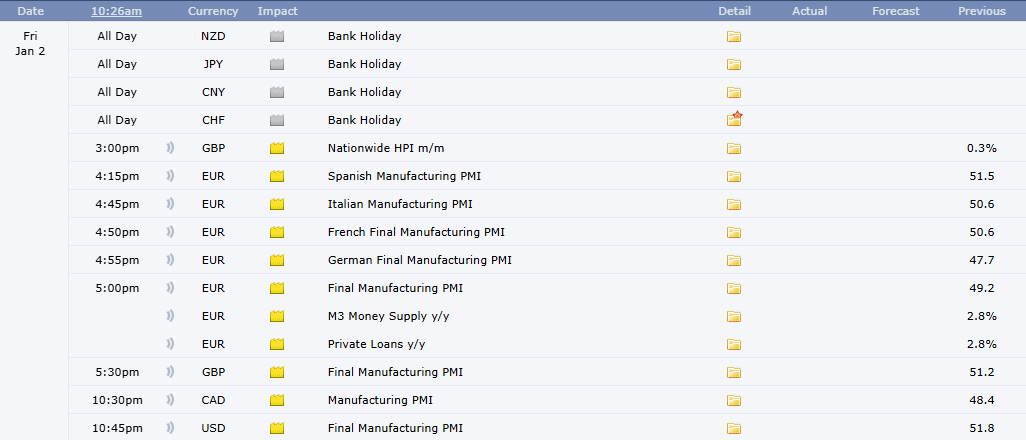

Today is all about the Purchasing Manager’s Index. In the US, the most recent flash PMI data for December 2025 showed that business activity growth slowed, with the composite PMI around 53.0, the weakest pace in six months. This was driven by slower expansion in both manufacturing and services activity, and new orders for goods fell for the first time in about a year. The S&P Global manufacturing PMI measured 51.8 for December, down from the prior month’s figure and slightly below the consensus forecast, indicating slower factory activity even though the sector remained in modest expansion territory. Earlier in 2025 the US manufacturing PMI had been higher with readings above 52 in mid‑year before slipping in the latter part of the year, while service sector PMI readings also showed a gradual moderation from the stronger growth seen earlier in the year. On balance this reflects an economy that is still growing but losing some momentum as demand pressures soften and input costs remain a concern for companies. For today’s release markets will be looking to see whether this trend continues, with expectations that PMI readings will remain close to these recent levels rather than swinging sharply higher or lower.

Across Europe recent PMI data painted a picture of modest expansion that has been weaker than in the United States. According to recent PMI surveys, business activity in the euro area has been slow and sluggish, dragged down by weakness in Germany’s manufacturing sector even as France and other economies showed some improvement. Household spending remained cautious, and government debt constraints limited fiscal support for growth. Europe’s PMI readings have hovered near the threshold of expansion with some months showing slower momentum in business activity and others indicating only slight improvements. Investors will be watching to see if business activity remains stable or shows signs of further slowing, particularly given the uneven growth patterns seen across the euro area throughout recent months.

In the United Kingdom the latest PMI data available before 2025 year end suggested that business activity had seen some slight recovery but remained fragile. The UK PMI rose slightly above 50 in December 2025, just above the level that separates expansion from contraction, reflecting only modest growth in business conditions. This came against a backdrop of weakening labor market conditions and slowing economic output that have prompted the Bank of England to cut interest rates in response to lower inflation and slower growth. Earlier in 2025, the UK PMI had been volatile with readings that dipped below fifty on several occasions, signaling contraction, before rising again in later months. The market will assess whether this modest growth trend has been sustained into the new year or if the more tentative conditions in the UK economy have continued to weigh on business activity.

Turning to Canada, PMI readings for the Canadian economy have shown a pattern of tepid expansion in 2025 with occasional soft points. The Canadian manufacturing PMI and services PMI surveys indicated growth around the threshold of expansion throughout much of the year, but with readings often closer to 50 than above 50, reflecting slow output growth and mixed business sentiment. Demand conditions have been uneven with resource and export sectors providing some support while domestic demand and consumer activity have shown signs of slowing. Recent PMI reports suggested that Canadian business activity continued at a modest pace as the economy grappled with higher borrowing costs and softer global demand. For the upcoming release Canadians and global investors alike will be interested to see if the Canadian PMI remains stable or shows a further slowdown given the challenges that have emerged over recent months.

It is also important to recognize that because the year has just started, many traders and financial institutions will still be in holiday mode with lower participation and reduced liquidity. Volatility will most likely return next week marking the official start of 2026 trading.

Analysis by Coach Angel

——

Disclaimer: Investing is risky. Investors should study the information before making investment decisions